Disclosure: The views and opinions expressed here are solely those of the author and do not represent the views and opinions of crypto.news editorial.

We started our new Outset Data Pulse analysis, expecting 12 years of major data to confirm a familiar belief in cryptocurrencies: that news moves markets, and that faster headlines give you an advantage.

But what are the results? Show Instead, it was more troubling: most of the time, the price seemed to move first, and the headline came later to explain it.

This does not mean that “the news does not matter.” It is akin to saying that we were treating it as the catalyst when it often acts like an explanation after the movement. It is easy to see why this belief has persisted for so long.

Anyone who spends enough time with cryptocurrencies starts to notice the same thing: something moves, the news feed lights up, and then the dots connect. When Bitcoin Pranks Or it goes up, coverage doubles. When a big decision comes out, whether it’s ETF approval, a stock market crash, or a legal victory, the headlines explode, too.

But the really important part of this belief – the part that turns news into a tradable advantage – is directional. If headlines really cause price action, reading faster gets you early. If price action is generating headlines, reading faster will often make you better informed about what actually happened.

That was the real question here: not whether news was in sequence, but whether it always came early enough to matter in the way traders often assumed.

The part where the data becomes more difficult to argue with

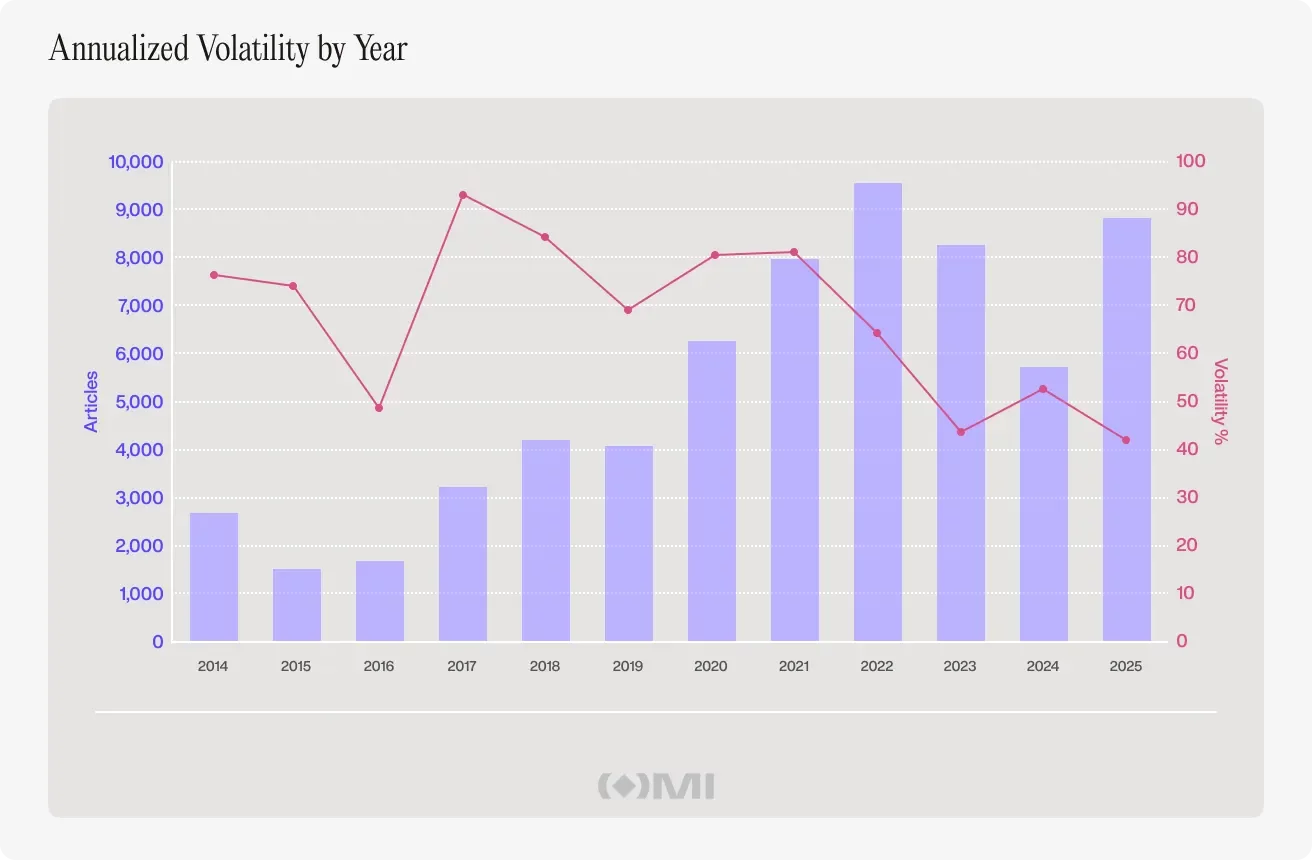

The underlying data set supporting this Outset Data Pulse report includes 63,926 major CoinDesk addresses spanning January 1, 2014 through December 30, 2025, matched to daily Bitcoin closing prices from the TradingView Composite Index.

This gave us 4,381 days for which the closing price and number of headlines were available – enough to test the relationship from several angles, including causality, price behavior around major news rallies, general sentiment, and topic clustering on the busiest coverage days.

It’s also broad enough to cover every “surely news is important out there” event worth experiencing, including bull and bear cycles, the FTX crash, the coronavirus crash, and the beginning of the spot Bitcoin ETF era.

News volume did not predict price

One of the first things we looked at was whether yesterday’s information helped predict today’s movement.

We examined five time horizons, from one to five days. What stuck out was that the news did not predict the price of Bitcoin during those time periods.

Then there’s the kind of number you can’t really argue with because it’s too small to seem significant: the correlation between daily article volume changes and daily Bitcoin returns was 0.019, meaning that only 0.04% of the daily price movement was explained. For practical purposes, this is effectively zero.

The long-term picture points in the same direction. Year after year, Bitcoin volume and volatility have moved at very different rhythms, with no stable relationship between heavier coverage and more explosive price behavior.

This does not mean that news and volatility never overlap. Clearly they do. But over time, the relationship remains too loose and inconsistent to treat heading size as a reliable signal on its own.

The price started to appear before the coverage

We also looked in the opposite direction: whether price movements tend to appear before key volume, and the most interesting pattern emerged around a two-day lag period.

But the part that seemed closest to the actual market experience was looking at the 50 biggest news days and tracking the Bitcoin price three days before and three days after each spike.

What stood out was the shape of the movement. In the three days leading up to the spike in coverage, the price of Bitcoin was already high, about 1% above the event day baseline. Then after rising, the price fell by about 0.8% on the third day.

This is not a “news moves markets” narrative. It’s a “markets move, then the news catches up” story. Once you see this look, you start to notice how many famous cryptocurrency moments seem to rhyme with it.

Even the big headlines were not clean signals

These are the moments we all remember because they were turning points for cryptocurrencies. For example, the US Securities and Exchange Commission approved the spot Bitcoin ETF on January 11, 2024. CoinDesk published 51 articles that day while Bitcoin fell 7.67% the next day and fell 10% on the third day.

Compare that with December 4, 2023, when speculation was running high but nothing was confirmed. CoinDesk published 81 articles, and Bitcoin rose 5% the next day.

The same discrepancy has appeared elsewhere: after the FTX collapse produced the busiest news day in the data set, Bitcoin barely moved, while a January 2017 breakout back above $1,000 was followed by an 11% decline the next day and nearly 20% within three days.

Across the ten largest news events in the data set, price reactions never settled into a usable pattern—some produced strong gains, others sharp losses, and many were never clearly followed through on.

This contradiction is important because it is what breaks the tradability story. If Market Action News were a stable indicator on a daily level, the biggest news spikes would be where you would expect the relationship to appear most clearly, and certainly not where it dissolves into randomness.

We also experienced emotions

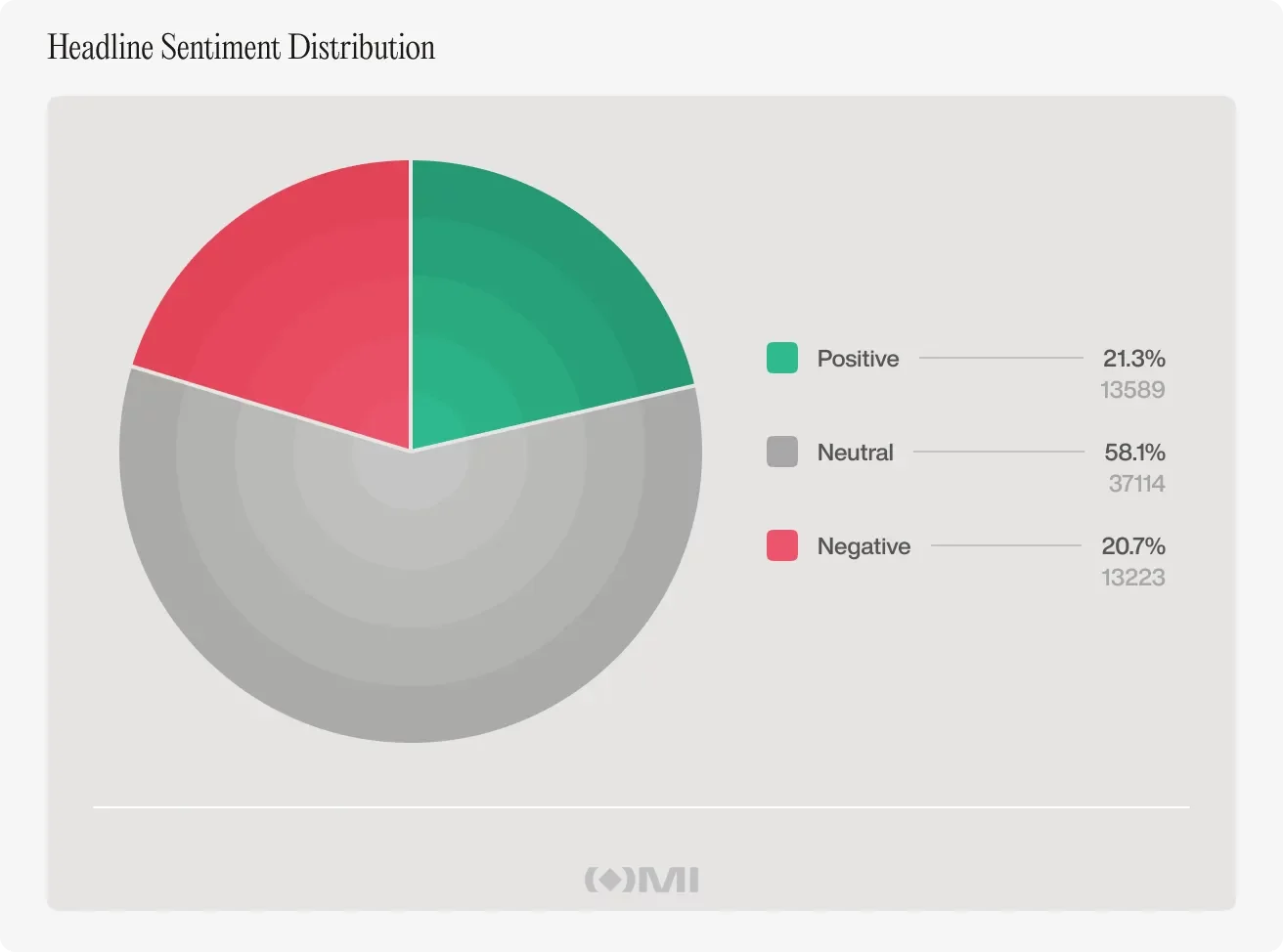

At this point, the obvious drawback is that volume is noisy, but sentiment may still be the best. Surely bullish versus bearish headlines must matter, right?

Therefore, each headline was propagated by the FinBERT financial sentiment model. Each title was classified as positive, negative, or neutral. Sentiments were also averaged across each day.

The distribution of the data set was almost perfectly balanced, with 58% neutral, 21% positive, and 21% negative. The important part of trading is the next step: Did the daily headline tone correlate with the daily returns?

The reported correlation was 0.07, with sentiment explaining about 0.5% of price movement. Again, this is close to nothing for anyone trying systematic time entries. Worse still (or perhaps more telling), the relationship was not stable. At three-month intervals, the relationship reversed between positivity and negativity with no consistent pattern.

There’s also something that seems obvious as soon as you say it out loud: key emotions can eventually “categorize” language that’s already racing to price. A headline like “Bitcoin Price Drops Below $70K” gets a negative score, but the decline is actually present in the price data on the same day.

We’re back in the same place: the title describes the movement, not its introduction.

Paraphrasing that made it all make sense

None of what we’ve seen so far falls into the “ignoring the news” category. This is not true, and it is not helpful.

The most optimistic twist is this: by the time the headline reaches a major publication, the information has already traveled through faster channels. This includes request flow, on-chain data, social layers, intranets, and other forms of positioning and interpretation that do not wait for editorial cycles.

This is the line that changes how we read the market. The media is not where the signal begins. It is where the signal becomes readable. Headlines are very much the “last mile,” marking the moment when a movement that has already started is named, mobilized, discussed, and turned into a story that people can repeat.

What does this change?

Reading faster doesn’t necessarily make you premature. The market absorbs information even before the newsroom approves the frame. Headlines are often better at telling us what just happened than what will happen next. This is not an insult to the press. It’s a statement about timing.

And using media as a timing tool can put you behind the market, because the thing you’re interacting with may already be reflected in your flows and positioning by the time you’re ready to act.

Even the report makes it clear: headlines are not just a clean signal. On the peak days of coverage, about 61% of the headlines fell into industry-wide hype — partnerships, fundraising, product launches, stablecoin development, NFT and gaming updates — with no clear connection to what’s next for Bitcoin. Even regulation, the strongest plausible category, still fails to produce a reliable signal at the day-to-day level.

One curious finding was that even Bitcoin halvings did not emerge as a distinct cluster on extreme news days, suggesting that some of Bitcoin’s most important forces do not operate through the daily main cycle at all.

Where we have to be honest about exceptions

News can be relevant in much shorter time frames, specifically minutes rather than days. The headline can still move the market at the moment, even if this effect is mitigated once you zoom out to daily closing prices.

At the same time, longer, slower narrative shifts, the kind that build up over weeks, may still affect price in ways that this approach cannot fully capture.

There are limits to this too: a single publication, even a highly authoritative one, does not represent the entire world of information. The fastest cryptocurrency information often travels through social platforms and private channels that this data set cannot track. Also, some patterns may only emerge in specific circumstances, and not in the cleaner, everyday relationships that these tests can detect.

So, we are left with a simple slogan that “news is useless.” Instead, we are left with something more actionable: most of the time, the headline is that the market has become explainable, not that the market is starting to move.