Nakamoto Holdings, the original Bitcoin conglomerate founded by BTC CEO David Bailey, sold nearly $20 million worth of Bitcoin at a realized loss of about 40%, a liquidation event that included an average acquisition cost of somewhere in the range of $33,000 per Bitcoin for a sale price consistent with market levels at the time of execution.

The deal was not framed as a routine portfolio rebalancing; A realized loss of 40% on a position of this size, for a company whose entire strategic identity is built around Bitcoin accumulation, suggests action that is forced or at least out of urgency.

For a company that raised more than $750 million in mid-2025 explicitly to build and hold Bitcoin treasury positions globally, selling at a significant loss raises immediate questions about liquidity management and the robustness of its financing model.

Bitcoin Treasury (NASDAQ: NAKA) disclosed in its 10K filing on March 30, 2026, that it sold approximately 284 bitcoins in March for about $20 million, with an average sale price of about $70,422 per bitcoin. In 2025, the company purchased 5,342 Bitcoin worth… pic.twitter.com/DRq8cpT0L6

— Wu Blockchain (@WuBlockchain) March 30, 2026

Nakamoto merged with healthcare provider KindlyMD in May 2025, securing a record $510 million PIPE along with additional debt financing, with Anchorage Digital handling custody. This structure is designed to return Bitcoin gains to the stack while maintaining a maximum public equity exposure of 40% – a structure that, in theory, insulates the Bitcoin stack from forced liquidation. A $20 million sale at a 40% loss indicates that architecture is under pressure it was not designed to absorb.

discovers: Meme Coin Supercycle: Best performer this week

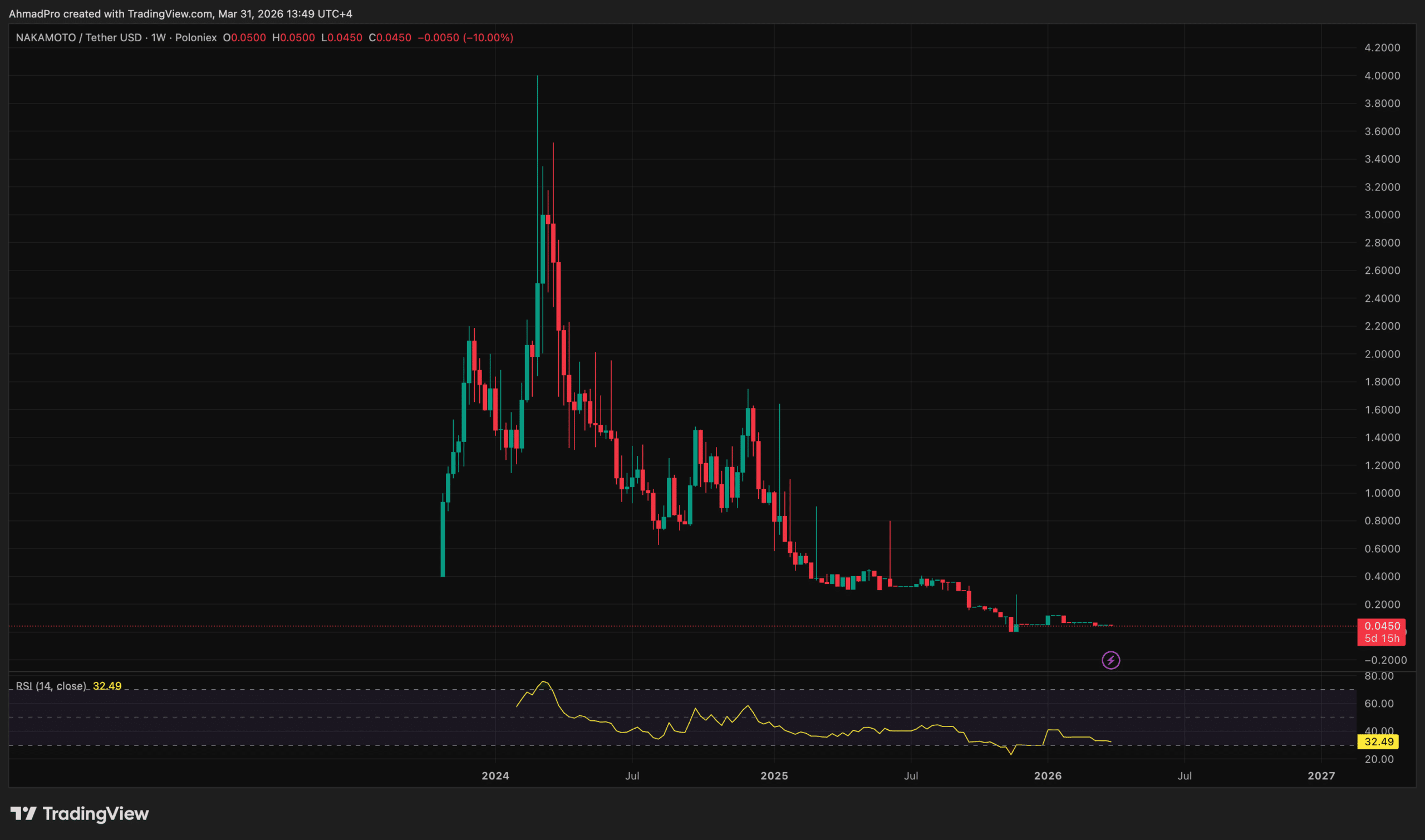

Implied acquisition cost versus realized exit price for Nakamoto Bitcoin Holdings

Based on the reported numbers, a 40% realized loss on a $20 million sale suggests that the position was executed at a cost basis of about $33.3 million — meaning Nakamoto actually made back $0.60 on every $1 posted in that tranche of Bitcoin.

If the selling occurred at Bitcoin prices in the $80,000 to $95,000 range, which characterized most of early to mid-2026, the implied acquisition price for this particular tranche would put the original purchase somewhere between $133,000 and $158,000 per coin — levels consistent with the peak of accumulation in late 2025 when treasuries were aggressively competing for spot supply.

David Bailey $now And Corey Klipsten $sequence They are trying their best to see who can lose the title of worst managed BTCTC https://t.co/RKa5o3VZLS pic.twitter.com/vuLRaltJBL

– Pledditor (@Pledditor) March 30, 2026

The exact means of sale – whether an OTC block, open market execution, or exchange liquidation – has not been confirmed and the on-chain footprint has not been independently verified by Arkham Intelligence or Lookonchain at the time of writing.

What the math clearly confirms: This was not tax loss harvesting on a marginal position. The realized loss of $13.3 million represents a significant destruction of capital for a company that positioned itself as a long-term holder of Bitcoin, rather than a commercial entity. The numbers crystallize a fundamental structural weakness – holding BTC near cycle highs with diluted or diluted equity capital leaves no margin for withdrawal without eventual forced realization.

explores: Cryptocurrency hack alerts this week

Balance sheet pressure and what liquidation reveals

Nakamoto’s financing model is based on mNAV arbitrage: issuing stocks or bonds at a premium to net asset value, spreading the proceeds into Bitcoin, and letting the appreciation in value expand the spread. This engine works in reverse when the stock collapses.

source: Tradingview

By early 2026, Nakamoto’s stock price had fallen roughly 99% from its peak in May 2025, effectively shutting down the ATM and pipeline channels that had provided accretion fuel. With equity-based financing no longer available at viable dilution rates, the company’s options narrow to servicing debt from cash reserves or liquidating Bitcoin holdings – the latter of which is precisely what this deal represents.

The contrast with other leveraged BTC treasury operators is beneficial. The strategy (MSTR) responded to market pressures by doubling down on additional capital raisingstends to increase its premiums to NAV while it holds.

In contrast, GameStop maintained its 4,710 BTC position Despite outside speculation about a sell-off – a situation that is only sustainable for companies without severe debt service obligations. Nakamoto’s realized loss indicates that it has neither the premium engine nor the unencumbered balance sheet to negatively absorb the decline.

Governance risks exacerbate balance sheet pressures. Nakamoto’s simultaneous acquisition of BTC Inc. Owned by Bailey and UTXO Management — using shares worth about $1.12 each after a 99% collapse — drew criticism from market watchers who described the moves as self-dealing at the expense of shareholders.

That a treasury company would sell bitcoin at a 40% loss while simultaneously acquiring its founder’s private assets is a combination that no amount of structuring bitcoin-denominated convertible securities can fully obscure.

discovers: Best Memecoins to Buy This Month!

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article aims to provide accurate and timely information but should not be considered financial or investment advice. Since market conditions can change rapidly, we encourage you to verify the information yourself and consult with a professional before making any decisions based on this content.

Daniel Francis is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. A crypto native since 2017, Daniel brings his background in cross-chain analytics to author evidence-based reports and detailed guides. It is certified by the Blockchain Council and is dedicated to providing “information gain” that cuts through the market noise to find blockchain’s real-world utility.