Brad Garlinghouse, CEO of Ripple and one of the most prominent voices in the institutional cryptocurrency space, appeared on Fox Business this week and accused Jamie Dimon, Chairman and CEO of JPMorgan Chase, of intentionally distorting a clarity law, the Digital Asset Market Clarity Act of 2025 (H.R. 3633), to protect a payments franchise that generates nearly $20 billion in annual revenue with estimated profits exceeding $5 billion.

The specific fault line is one provision in pending legislation that would allow cryptocurrency exchanges to offer stablecoin returns to users, a provision that Dimon has publicly opposed and that the banking lobby has identified as its primary legislative target.

This is not just a dispute over regulatory philosophy or compliance architecture. It is a structural contest over who controls the next generation of dollar-denominated digital payment instruments, and whether these instruments will operate as pure transaction channels, which is the outcome favored by the banking sector, or as yield products that compete directly with bank deposits for household money.

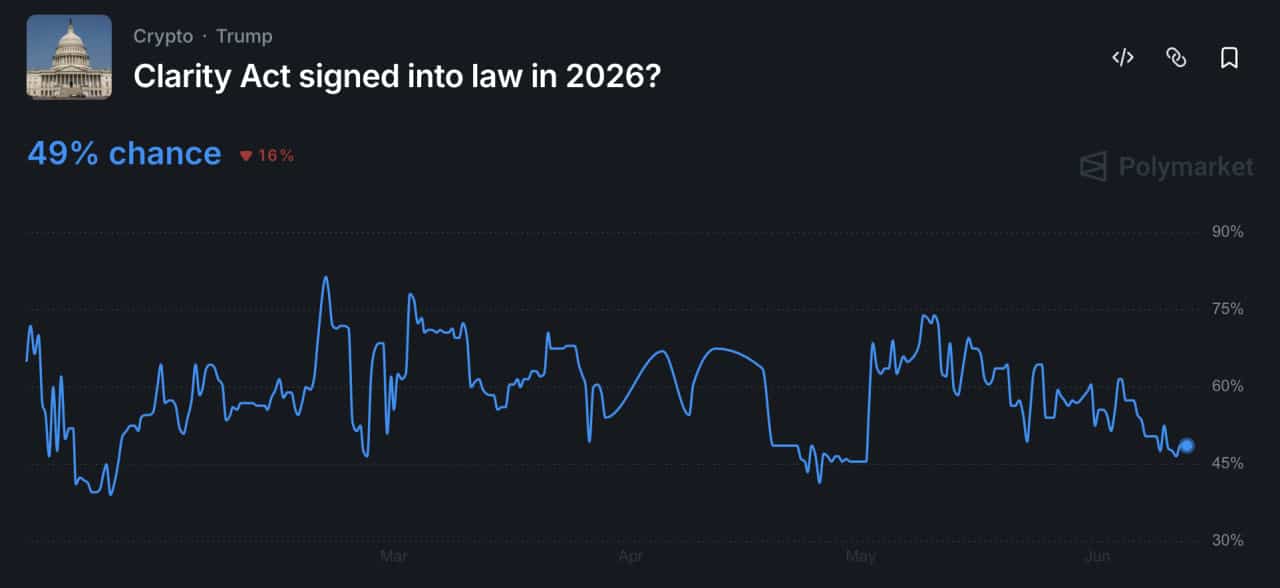

source: Polymarket

Polymarket prediction market users are currently assigning odds of 49% for the Clarity Act to be signed into law this year, down about 18 percentage points from the previous week, a pressure that reflects the real uncertainty created by this specific break between industries.

explores: The next crypto to explode in Q2

Opposing Dimon: JPMorgan’s $20 billion payments concession, his specific public arguments against the provision, and the structural logic behind the bank’s resistance to the Clarity Rule

Jamie Dimon’s opposition to the stablecoin return requirement in the Clarity Act has been publicly stated in several guises, most recently in an interview with Fox Business host Maria Bartiromo, the same format and interview in which Dimon previously targeted Brian Armstrong, co-founder and CEO of Coinbase, over Armstrong’s defense of the bill.

In a previous appearance in May, Dimon described Armstrong as “the only person” pushing for the inclusion of stablecoin returns, claimed that Coinbase was spending “hundreds of millions of dollars in Washington” on the effort, and concluded that Armstrong was, in Dimon’s words, “full of shit.” Dimon’s more recent comments, to which Garlinghouse was responding directly, claimed that the Clarity Act reduces compliance safeguards and creates conditions under which illegal activity becomes easier.

Jamie Dimon, CEO of JPMorgan: “We will fight the Clarity Act. If we lose, we will lose, and we will survive. But it will be fought.”

“No one will bow down to Brian Armstrong or Coinbase…they are full of evil things.” pic.twitter.com/okbuiu2Q0s

– Altcoin Daily (@AltcoinDaily) May 29, 2026

The epistemological status of the exact $20 billion figure deserves attention. JPMorgan does not separate its payments revenue as a standalone public reporting line in a way that allows for rigorous verification, but the volume estimate is consistent with the company’s disclosed wholesale and consumer payments activity and is treated by analysts covering the sector as a reasonable approximation of the franchise at risk.

The structural logic of bank resistance is not difficult to reconstruct from publicly available materials. The American Bankers Association and the Banking Policy Institute issued a joint statement formally opposing the yield provisions earlier this year, arguing that yielding stablecoins would act as a substitute for deposits, pulling household savings out of the banking system and reducing credit intermediation capacity that regulators and community banks alike have cited as a systemic concern.

We believe that Dimon’s stated objections, framed in terms of compliance concerns and the risks of facilitating a bad actor, do not accurately reflect the underlying business motivation behind JPMorgan’s opposition, and that Garlinghouse’s franchise protection argument is the most analytically honest account of what is at stake for the bank.

A White House Council of Economic Advisers report published in April 2026 found that eliminating stablecoin yields entirely would increase bank lending by just $2.1 billion, a 0.02% increase in total credit supply, while imposing an estimated $800 million net welfare cost on consumers, a ratio that does not support the systemic risk framing that Dimon has publicly deployed.

The same analysis found that large banks would capture 76% of any additional lending that could be enabled by a yield ban, with community banks capturing the remaining 24%, a distribution that identifies precisely who benefits most from the regulatory outcome Dimon is calling for.

discovers: Best coins to buy in 2026

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article aims to provide accurate and timely information but should not be considered financial or investment advice. Since market conditions can change rapidly, we encourage you to verify the information yourself and consult with a professional before making any decisions based on this content.

Daniel Francis is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. A crypto native since 2017, Daniel brings his background in cross-chain analytics to author evidence-based reports and detailed guides. It is certified by the Blockchain Council and is dedicated to providing “information gain” that cuts through the market noise to find blockchain’s real-world utility.